Skip to main content

Skip to main content

Starting October 1: Some business services are now subject to retail sales tax, as required by state law, ESSB 5814. When you buy these services, vendors should add sales tax to your bill. If you sell these services, you should begin collecting retail sales tax. Learn more about Services newly subject to retail sales tax.

Tax incentive programs

Many businesses may qualify for tax incentives offered by Washington. These incentives include deferrals, reduced B&O rates, exemptions, and credits.

Your annual filing requirement

If your business claimed or plans to claim a tax incentive, you may be required to file an Annual Tax Performance Report. You must file the report by May 31 following each year you are eligible for the incentive. If May 31 falls on a weekend or state holiday, your due date is the next business day. If you do not file reports on time, 35% or 50% of the incentive you claimed becomes immediately due and payable.

The Annual Tax Performance Report is available to file in my My DOR starting April 1. If you cannot find the report online or have questions about an extension, contact Taxpayer Account Administration at 360-705-6210.

Check each tax incentive below for information on your reporting requirements.

Incentive area resources

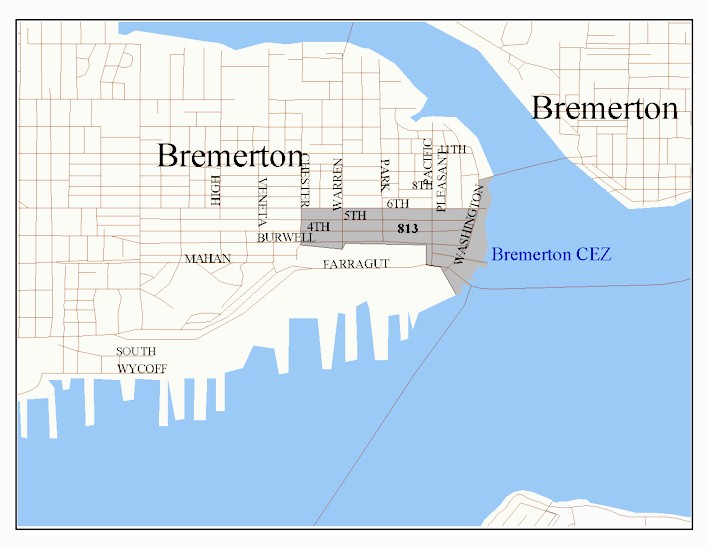

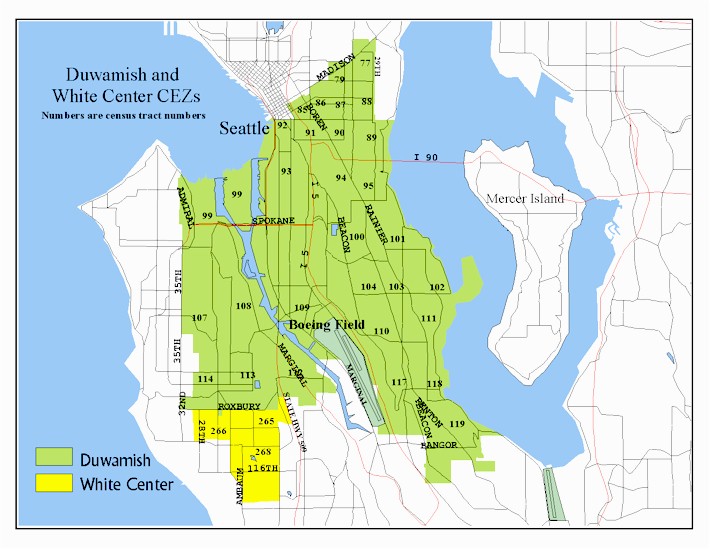

Community Empowerment Zone (CEZ) maps:

See if your business is in a CEZ. Enter the address in our Tax Rate Lookup Tool.

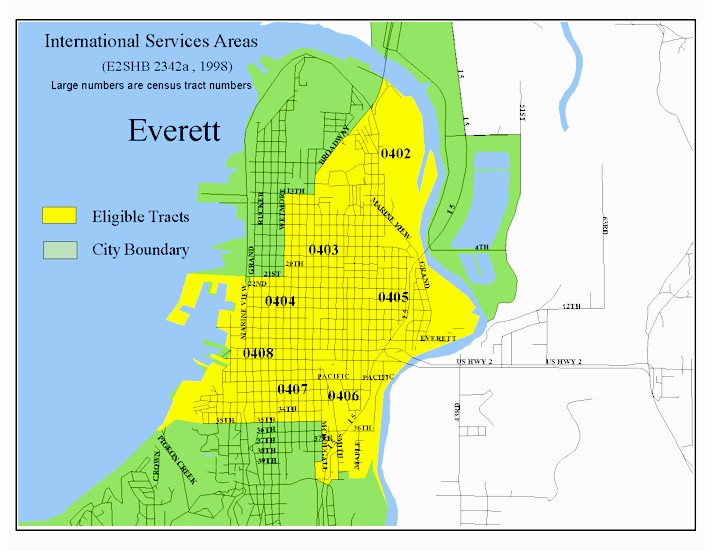

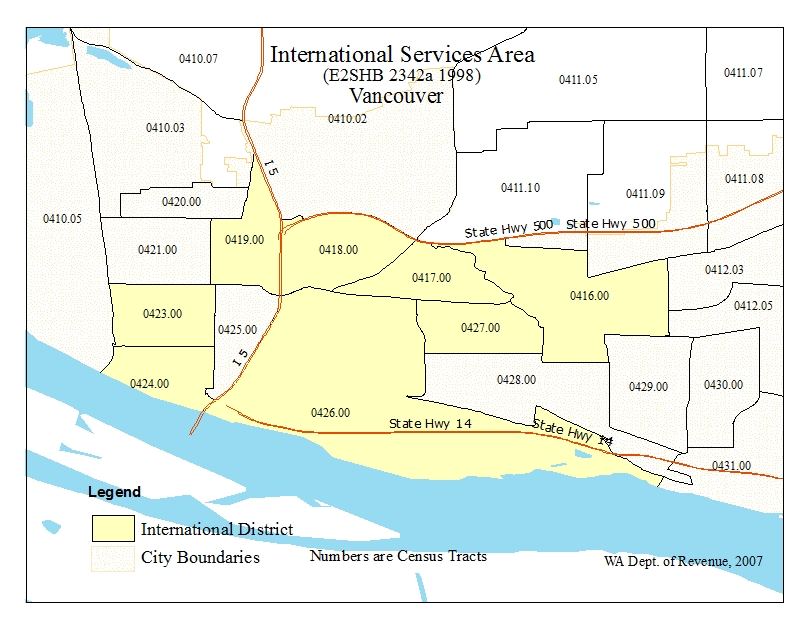

International service district maps:

List of rural counties (from OFM)

Incentives

Aerospace Industry

- B&O credit for preproduction development expenditures

-

Available to:

- Manufacturers and processors for hire of commercial airplanes or component parts of commercial airplanes.

- Non-manufacturers engaged in the business of aerospace product development.

- Certified FAR repair stations.

- Aerospace tooling manufacturers.

Qualifying activity:

Performing research, design and engineering activities to develop an aerospace product or aerospace product line. Activities must be performed in Washington to qualify for this credit.

Aerospace product:

Aerospace products are any of the following:

- Commercial airplanes and their components (including derivatives).

- Machinery and equipment designed and used primarily for maintenance, repair, overhaul, or refurbishing of commercial airplanes and their components by an FAR part 145 certified repair station.

- Tooling specifically designed for use in manufacturing commercial airplanes and their components.

Note: You must have documentation showing that the product you are working on is an aerospace product or that you are in the process of acquiring FAA certification for commercial airplanes or their components. You are not required to have an FAA air-worthiness certificate during development to qualify for the credit for commercial airplanes or their components.

Reporting/documentation:

- No application required.

- Aerospace Credit for Aerospace Product Development Spending worksheet completed for each reporting period the credit is taken. This worksheet is part of the online return.

- Annual Tax Performance Report filed by May 31 of each year after year when you claim the credit.

- Electronic filing required.

Expires July 1, 2040.

For questions about the credit, call Taxpayer Account Administration at 360-705-6216.

- B&O credit for property/leasehold taxes paid on aerospace business facilities

-

Available to:

- Manufacturers and processors for hire of commercial airplanes or component parts of commercial airplanes.

- Non-manufacturers engaged in the business of aerospace product development.

- Certified FAR repair stations.

- Aerospace tooling manufacturers.

Qualifying activity:

For manufacturers and processors for hire:

- Payment of property/leasehold taxes on new buildings, land, and the increased value of renovated buildings used exclusively in manufacturing commercial airplanes or components of such airplanes; or in manufacturing tooling specifically designed for use in manufacturing commercial airplanes or components of such airplanes.

- Payment of property taxes on equipment eligible for the machinery and equipment (M&E) exemption multiplied by a fraction for qualifying use.

For certified FAR repair stations and aerospace non-manufacturers:

- Payment of property/leasehold taxes on new buildings, land, and the increased value of renovated buildings used exclusively in aerospace product development or in providing aerospace services.

- Payment of property taxes on qualifying computer equipment and peripherals used primarily in aerospace product development or in providing aerospace services.

Reporting/documentation:

- No application required.

- Annual Tax Performance Report filed by May 31 of the following year.

- Electronic filing required.

Expires July 1, 2040.

For questions about the credit, call the Taxpayer Account Administration Division within DOR at 360-705-6216.

- B&O tax rate for aerospace businesses

-

Effective April 1, 2020, Engrossed Senate Bill 6690 repealed the aerospace preferential rates in RCW 82.04.260(11). Businesses no longer report under the following line codes:

- Manufacturing of Commercial Airplanes, Components, or Aerospace Tooling.

- Wholesaling of Commercial Airplanes, Components, or Aerospace Tooling.

- Retailing of Commercial Airplanes, Components, or Aerospace Tooling.

Aerospace manufacturers of commercial airplanes and components of commercial airplanes

B&O tax rates for manufacturers of commercial airplanes and manufacturers of components for commercial airplanes increased effective April 1, 2020. If you manufacture commercial airplanes or components for commercial airplanes you should report under the following line codes:

- Manufacturing of Commercial Airplanes or Components (0.484%).

- Wholesaling of Commercial Airplanes or Components (0.484%).

- Retailing of Commercial Airplanes or Components (0.484%).

Aerospace tooling manufacturers

B&O tax rates for manufacturers of tooling increased effective April 1, 2020. If you manufacture tooling specifically designed for use in manufacturing commercial airplanes or components of commercial airplanes, you should report as follows:

- From April 1, 2020 to Dec. 31, 2020, under the standard B&O tax classifications for manufacturing, processing for hire, wholesaling, and retailing.

- Beginning Jan. 1, 2021, under the following classifications:

- Manufacturing of Commercial Airplane Tooling (0.484%).

- Wholesaling of Commercial Airplane Tooling (0.484%).

- Retailing of Commercial Airplane Tooling (0.471%).

Please see ESB 6690 for more information.

Aerospace non-manufacturers

If you are performing aerospace product development for others you should report under the B&O tax classification Non-manufacturing Aerospace Product Development at a preferential rate of 0.9%.

Note: This is an apportionable activity.

The preferential rate expires June 30, 2040.

Federal Aviation Administration (FAR) Part 145 Repair Stations

If you are a certified FAR part 145 repair station you should report under the B&O tax classification Federal Aviation Administration (FAR) Repair Station at a preferential rate of .2904% for retail sales that are exempt from sales tax under RCW 82.08.0261, RCW 82.08.0262, or RCW 82.08.0263.

Note: For all other sales you should report under the standard Wholesaling or Retailing B&O tax classifications and rates.

The preferential rate expires June 30, 2040.

Reporting/documentation:

The following reporting/documentation requirements apply to the preferential B&O tax rates and other aerospace incentives.

- No application required.

- Annual Tax Performance Report filed by May 31 of the following year.

- Electronic filing required.

For questions about the reporting of aerospace, call the Taxpayer Account Administration Division within DOR at 360-705-6216.

- Construction of new facilities used for airplane repair and maintenance - retail sales/use tax exemption

-

Available to:

- Eligible maintenance repair operator engaged in the maintenance of airplanes.

- Port district, political subdivision, or municipal corporation building and leasing facilities to an eligible maintenance repair operator engaged in the maintenance of airplanes.

Qualifying activity:

Construction of new buildings to be used for airplane repair and maintenance including:

- Labor and services used to construct new buildings.

- Materials used as an ingredient or component during construction.

- Labor and services to install building fixtures that do not qualify for the manufacturer’s machinery and equipment sales and use tax exemption under RCW 82.08.02565.

The exemption is in the form of a refund. Applicants must pay the state and local sales taxes at the time of purchase and then apply for a refund. Businesses may only submit one application per calendar quarter.

Reporting/documentation:

- Completed Application for Refund or Credit with other documents outlined in the Special Notice.

- Annual Tax Performance Report filed by May 31 of each year following a year in which you received a refund.

- Electronic filing required.

Expires January 1, 2031.

For questions about the exemption, call Taxpayer Account Administration at 360-705-6216.

- Retail sales and use tax exemption for the construction of new facilities used to manufacture commercial airplanes, fuselages or wings of commercial airplanes

-

Available to:

- Manufacturers of commercial airplanes, fuselages, and wings.

- Port districts, political subdivisions, or municipal corporations who lease facilities to these manufacturers.

Qualifying activity:

Constructing new buildings and/or new additions to buildings primarily used to manufacture commercial airplanes, commercial airplane fuselages and commercial airplane wings as defined in RCW 82.32.550 and RCW 82.32.850.

Reporting/documentation:

- No application required.

- Completed Buyer's’ Retail Sales Tax Exemption Certificate for vendor.

- Annual Tax Performance Report filed by May 31 of the following year.

- Buyer completes Buyers Sales and Use Tax Preference Addendum in My DOR when filing their tax return.

- Electronic filing required.

Expires July 1, 2040.

For questions about the exemption, call Taxpayer Account Administration at 360-705-6216.

- Sales & use tax exemption for aerospace businesses for computer hardware/software/peripherals

-

Available to:

- Manufacturers and processors for hire of commercial airplanes or component parts of commercial airplanes.

- Non-manufacturers engaged in the business of aerospace product development.

- Certified FAR repair stations.

- Aerospace tooling manufacturers.

Qualifying activity:

Purchases of computer hardware, software, and peripherals, and charges for labor and services related to the installation of such equipment. The hardware, software, and peripherals must be primarily used in the development, design, and engineering of aerospace products or in providing aerospace services.

Reporting/documentation:

- No application required.

- Completed Buyer's’ Retail Sales Tax Exemption Certificate for vendor.

- Annual Tax Performance Report filed by May 31 of the following year.

- Buyer completion of Buyers Sales and Use Tax Preference Addendum in My DOR when filing their tax return.

Expires July 1, 2040.

For questions about the exemption, call Taxpayer Account Administration at 360-705-6216.

Aluminum Smelting Industry

- B&O tax credit for property tax on aluminum smelter

-

Available to:

An aluminum smelter who manufactures aluminum in this state.

Qualifying activity:

B&O tax credit for property tax paid by an aluminum smelter.

Reporting/documentation:

- No application

- A person must pay the tax and may then take a credit equal to the property tax paid.

- Annual Tax Performance Report must be filed by May 31st of the following year.

- Electronic filing of all documents required.

For questions about the credit, call Taxpayer Account Administration at 360-705-6214.

- B&O Tax/Public utility tax credit for electricity, natural gas, or manufactured gas sold to aluminum smelters

-

Available to:

A person who sells electricity, natural gas or manufactured gas to an aluminum smelter in Washington State.

Qualifying activity:

To qualify for the credit a person must sell electricity, natural gas, or manufactured gas to an aluminum smelter. The credit is equal to the gross amount of sales to the aluminum smelter multiplied by the corresponding rate of Business & Occupation (B&O) Tax and/or Public Utility Tax (PUT) but only when it’s specified in a contract that the price of the electricity or gas sold to the smelter will be reduced by an amount equal to the credit.

Reporting/documentation:

- Completion of Credit for Energy Providers to Aluminum Smelters.

- No Annual Tax Performance Report required.

- Electronic filing not required.

For questions about the credit, call Taxpayer Account Administration at 360-705-6214.

- Brokered natural gas use tax exemption

-

Available to:

Aluminum smelters who manufacture aluminum in this state.

Qualifying Activity:

Use tax exemption for the use of natural or manufactured gas by an aluminum smelter.

Reporting/documentation:

- No application.

- Annual Tax Performance Report must be filed by May 31st of the following year.

- Electronic filing of all documents required.

For questions about the exemption, call Taxpayer Account Administration at 360-705-6216.

- Reduced B&O tax rate for aluminum smelting

-

Available to:

Aluminum smelters and processors for hire who manufacture aluminum in this state.

Qualifying activity:

Manufacturing aluminum and selling the same at wholesale by aluminum smelters and processors for hire.

Reporting/documentation:

- No application.

- Annual Tax Performance Report must be filed by May 31st of the following year.

- Electronic filing of all documents required.

For questions about the program, call Taxpayer Account Administration at 360-705-6214.

- Retail sales tax credit for state portion of sales tax paid on materials, equipment, labor and services used in aluminum smelting

-

Available to:

Aluminum smelters and processors for hire who manufacture aluminum in this state.

Qualifying activity:

Retail sales tax credit for personal property used at an aluminum smelter, tangible personal property that will be incorporated as an ingredient or component of buildings or other structures at an aluminum smelter, or for labor and services rendered with respect to such buildings, structures, or personal property.

Reporting/documentation:

- No application

- Person must pay the tax and may then take a credit equal to the state share of retail sales tax paid.

- Annual Tax Performance Report must be filed by May 31st of the following year.

- Electronic filing of all documents required.

For questions about the credit, call Taxpayer Account Administration at 360-705-6214.

Biofuel Industry

- Property/leasehold tax exemption for manufacturers of biofuels

-

Available to:

Manufacturers of alcohol fuel, biodiesel fuel, biodiesel feedstock, or wood biomass fuel.

Qualifying activity:

Manufacturing alcohol fuel, biodiesel fuel, biodiesel feedstock, or wood biomass fuel.

Reporting/documentation:

- Application for exemption must be made by November 1 to local county assessor.

- No Annual Tax Performance Report.

- Electronic filing not required.

- No claims may be filed after December 31, 2015.

For questions about the exemption, contact your local county assessor's office.

- Reduced B&O tax rate for manufacturing wood biomass fuel

-

Available to:

Manufacturers of wood biomass fuel.

Qualifying activity:

Manufacturing wood biomass fuel.

Reporting/documentation:

- No application.

- No Annual Tax Performance Report.

- Electronic filing not required.

Expires January 1, 2029.

For questions about the program, call 360-705-6705.

- Waste vegetable oil - Sales/use tax exemption on purchases for personal use

-

Available to:

Any person that is not engaged in selling biodiesel fuel at wholesale or retail.

Qualifying activity:

Purchase of waste vegetable oil to produce biodiesel fuel for personal use. Waste vegetable oil is used cooking oil gathered from restaurants or commercial food processors.

Reporting/documentation:

- Buyer must provide seller with Buyers’ Retail Sales Tax Exemption Certificate.

- No application.

- No Annual Tax Performance Report.

- Electronic filing not required.

For questions about the sales and use tax exemption, call 360-705-6705.

Data Centers

- Rural data centers - Sales/use tax exemption for purchases of server equipment and power infrastructure

-

Available to:

Available to the owner and tenants of an eligible data center that has a combined square footage of at least 100,000 square feet and is located in a rural county.

Qualifying activity:

Construct, renovate, or expand a data center under a building permit issued during one of the following periods:

- April 1, 2010 to June 30, 2011.

- April 1, 2012 to June 30, 2015.

- July 1, 2015 to June 30, 2036.

Or, refurbish an existing facility.

Refurbishment means a substantial improvement to an eligible computer data center. Certificates for refurbishment are limited to six each calendar year. Each qualifying business may only apply for one refurbishment certificate per data center per calendar year.

Sales/use tax exemption on:

- Purchases of eligible server equipment and labor and services to install server equipment, in an eligible data center.

- Purchases of eligible power infrastructure, and labor and services to construct, install, repair, alter, or improve eligible power infrastructure.

Employment requirements:

Within six years of the issuance of an exemption certificate, the owner or tenant must show net employment increased by a minimum of the lesser of:

- 35 family wage employment positions.

- Three family wage employment positions for each 20,000 square feet or less of newly dedicated server space at the eligible computer data center.

For tenants, the increase of family wage jobs is based only on the space occupied by the tenant.

Construction requirements:

Within three years after being placed in service, a qualifying business operating a newly constructed data center must certify to the department that it has obtained certification under one or more specified sustainable design or green building standards.

Application process:

- Review the List of Rural Counties for eligibility.

- Submit the appropriate Application for Sales Tax Exemption for Purchases by Data Centers before purchasing server equipment or power infrastructure.

Approval and reporting:

- If approved, the department will issue a Certificate for Sales Tax Exemption for Purchases by Data Centers.

- Once approved, you must submit all of the following:

- The Annual Tax Performance Report by May 31 of the year following any year in which an exemption is taken.

- The Buyer’s Sales and Use Tax Preference Addendum each tax reporting period on your excise tax return, to disclose the amount of purchases made using the exemption certificate.

All documents must be submitted electronically.

Expires July 1, 2048.

For questions about the application, call Taxpayer Account Administration at 360-705-6217.

- Urban data centers - Sales/use tax exemption for purchases of server equipment and power infrastructure

-

Available to:

Available to the owner and tenants of an eligible data center that has a combined square footage of at least 100,000 square feet and is located in King, Pierce, or Snohomish County.

Qualifying activity:

To qualify, the data center must have a building permit to construct, renovate, or expand the data center issued after June 9, 2022, or refurbish an existing facility.

Refurbish means a substantial improvement to an eligible computer data center.

Sales/use tax exemption on:

- Purchases of eligible server equipment and labor and services to install server equipment, in an eligible data center.

- Purchases of eligible power infrastructure, and labor and services to construct, install, repair, alter, or improve eligible power infrastructure.

Limit on number of certificates:

The department is limited in the number of certificates it can issue as follows:

Calendar Year 2022 2023 2024 2025 2026 2027 Number of certificates 6 0 6 6 6 6 Employment requirements:

Within six years of the issuance of an exemption certificate the owner or tenant must show net employment increased by a minimum of three family wage employment positions for each 20,000 square feet or less of newly dedicated server space at the eligible computer data center.

For tenants, the increase of family wage jobs is based only on the space occupied by the tenant.

Construction requirements:

Within three years after being placed in service, a qualifying business operating a newly constructed data center must certify to the department that it has obtained certification under one or more specified sustainable design or green building standards.

Application process:

Submit the appropriate Application for Sales Tax Exemption for Purchases by Data Centers before purchasing server equipment or power infrastructure.

Approval and reporting:

- If approved, the department will issue a Certificate for Sales Tax Exemption for Purchases by Data Centers.

- Once approved, you must submit all of the following:

- The Annual Tax Performance Report by May 31 of the year following any year in which an exemption is taken.

- The Buyer’s Sales and Use Tax Preference Addendum each tax reporting period on your excise tax return, to disclose the amount of purchases made using the exemption certificate.

All documents must be submitted electronically.

Expires July 1, 2038.

For questions about the application, call Taxpayer Account Administration at 360-705-6217.

Employer

- Commute trip reduction program - B&O tax/public utility tax credit (expired July 1, 2025)

-

Available to:

Employers and property managers. The accrual period for a property manager that provides incentives to persons employed at a worksite managed by the property manager expired on December 31, 2023.

Qualifying activity:

Providing commute trip reduction incentives to or on behalf of employees.

Reporting/documentation:

- Applications no longer accepted as of January 31, 2025.

- Credit must be claimed electronically through My DOR.

Program expired July 1, 2024, for property managers, and July 1, 2025, for employers. No credits may be applied to returns filed after June 30, 2025, even if they relate to prior tax periods.

- Hiring unemployed veterans - B&O tax and PUT credit (expired July 1, 2023)

-

Available to:

Businesses hiring unemployed veterans located in Washington.

Qualifying activity:

Employ a qualified employee for a full-time position located in Washington for at least two consecutive full calendar quarters on or after Oct. 1, 2016 and before June 30, 2022.

Credit cap and end date:

- Individual cap - 20% of the wages and benefits paid to the qualified employee not to exceed $1,500 per qualified employee.

- Credits may be earned through June 30, 2022.

- No credits may be claimed after June 30, 2023.

- Credits are available on a first-in-time basis. Statewide cap - $500,000 per fiscal year.

Reporting/documentation:

- You may claim the credit on your electronic excise tax return, if the qualified employee has been employed by you in Washington for at least two consecutive full calendar quarters.

- The amount of credit you claim during a reporting period cannot be more than the amount of your B&O tax and PUT owed during that period.

- Credits may be carried over until used, but must be claimed on returns filed no later than June 30, 2023.

- Credits will not be refunded.

- The online Annual Tax Performance Report is required by May 31 each year following the calendar year in which the tax incentive is claimed.

For questions about the credit, call Taxpayer Account Administration at 360-705-6214.

- International Services - B&O tax credit for new employment (repealed effective Jan. 1, 2026)

-

Available to:

Persons providing international services, such as computer; data processing; information; legal; accounting and tax preparation; engineering; architectural; business consulting; business management; public relations and advertising; surveying; geological consulting; real estate appraisal; or financial services in designated geographical areas.

Qualifying activity:

Creating permanent full-time positions in international services located in a Community Empowerment Zone (CEZ) or designated International Services District. International services must be provided to persons domiciled outside the United States or be for use primarily outside this country.

Do existing employees qualify for the tax credit?

Yes, if an existing employee moves into a newly created employment position that provides international services, and their previous position is filled by a new hire.

The tax credit is only available for newly created positions. In all cases, the position that generates the tax credit must be from a new one – not simply the result of reassigning existing staff.

Credit amount:

The amount of the credit is $3,000 per year for each qualified employment position created. If an eligible position is created after July 1 of a given year, the credit is reduced to $1,500 for that year.

How does a business take the tax credit?

A business that has earned the credit may claim it under the “Credits” section of the Combined Excise Tax Return. The credit claimed cannot be more than the B&O tax due.

Does the credit have to be used in the year it is earned?

No. The credit can be accrued and carried over until it is used. However, the credit amount cannot be refunded.

Reporting/documentation:

- No application.

- No Annual Tax Performance Report.

- Electronic filing not required.

- Maintain records necessary for the department to verify eligibility:

- Employment records for the previous six years;

- Information relating to description of international service activity engaged in at the eligible location by the person; and

- Information relating to customers of international service activity engaged in at that location by the person.

Note: This credit is repealed effective Jan. 1, 2026. The credit is calculated based on the entire 2026 fiscal year (Jul. 1, 2025-Jun. 30, 2026) but cannot be claimed after Dec. 31, 2025.

For questions about the credit, call Taxpayer Account Administration at 360-705-6214.

- Washington customized employment training program - B&O tax credit

-

Available to:

All Washington employers.

Qualifying activity:

Payments to the Employment Training Finance Account through the Customized Employment Training Program for customized employee training.

Credit equals 50% of payment to Employment Training Finance Account.

Reporting/documentation:

- Application with the State Board for Community and Technical Colleges for training allowance.

- Employment Credit Training Worksheet must be filed when claiming credit on return.

- Annual Tax Performance Report required by May 31st of the following year.

- Electronic filing of all documents required.

Program expires July 1, 2026.

No credits may be applied to returns filed after June 30, 2026, even if they relate to prior tax periods.

For questions about the credit, call Taxpayer Account Administration at 360-705-6214.

For questions about the program, visit the State Board for Community & Technical Colleges.

Extracting & Timber Manufacturing

- Reduced B&O tax rate for timber extracting and manufacturing

-

Extended to June 30, 2045 and expanded to include the manufacturing of mass timber products

Available to:- Extractors and extractors for hire of timber.

- Manufacturers and processors for hire of:

- Timber into timber products or wood products.

- Timber products into other timber products or wood products.

- Mass timber products.

- Sellers of standing timber.

Qualifying activity:

- Extracting timber or extracting timber for hire.

- Manufacturing or processing for hire of:

- Timber into timber products or wood products.

- Timber products into other timber products or wood products.

- Mass timber products as defined in RCW 19.27.570.

- Selling at wholesale:

- Timber extracted by the seller.

- Timber products manufactured by the seller from timber or other timber products.

- Wood products manufactured by the seller from timber or timber products.

- Mass timber products manufactured by the seller.

- Sales of standing timber, apart from the land, where the buyer is required to sever the timber within 30 months.

Reporting/documentation:

- No application required.

- Annual Tax Performance Report required by May 31st of the following year.

- Electronic filing of all documents required (except small harvesters).

For questions about the program, call 360-705-6705.

Farming & Agriculture

- Sales/Use tax exemption for anaerobic digesters

-

Available to:

Farmers and businesses establishing or operating anaerobic digesters.

Note: Beginning July 1, 2018, anaerobic digesters no longer have to be used primarily (more than 50%) to treat livestock manure.

Qualifying activity:

Purchases of tangible personal property that becomes an ingredient or component of the anaerobic digester and charges for installing, repairing, constructing, cleaning, altering or improving the anaerobic digester.

Reporting/documentation:

- Qualifying businesses must provide their vendors with a completed Farmers’ Certificate for Wholesale Purchases and Sales Tax Exemptions or a Buyers' Retail Sales Tax Exemption Certificate.

- No Annual Tax Performance Report.

- Electronic filing is not required.

- Record keeping requirements.

For questions about the program, call Kurt Sand at 360-705-6659.

- Sales/Use tax exemption for equipment to reduce field burning & construction of hay sheds (expired January 1, 2011)

-

Available to:

Qualified farmers.

Qualifying activity:

Purchase or use of certain equipment. The exemption is also available for materials, labor, and services for the construction of hay sheds.

Reporting/documentation:

- Qualified farmer must provide vendor with Farmers’ Retail Sales Tax Exemption Certificate.

- No Annual Tax Performance Report.

- Electronic filing not required.

- Proper record keeping required.

For questions about the exemption, call Kurt Sand at (360) 705-6659.

- Sales/Use tax exemption for farm fuel users

-

Available to:

Farmers producing agricultural products and persons providing horticultural services to farmers.

Qualifying activity:

Purchases of diesel fuel, biodiesel fuel, or aircraft fuel.

Reporting/documentation:

- Buyer provides Farmers Retail Sales Tax Exemption Certificate to seller.

- No Annual Tax Performance Report.

- Electronic filing is not required.

For questions about the program, call Kurt Sand at (360) 705-6659.

- Sales/Use tax exemption for livestock nutrient management equipment & facilities

-

Available to:

Licensed dairies with certified dairy nutrient management plans and qualifying animal feeding operations.

Qualifying activity:

Purchases that become an ingredient or component of existing livestock nutrient management equipment and facilities or services provided for operating, repairing, cleaning, altering, or improving this equipment and facilities.

Reporting/documentation:

- Qualifying businesses must provide their vendors with a completed Farmers’ Certificate for Wholesale Purchases and Sales Tax Exemptions.

- No Annual Tax Performance Report.

- Electronic filing is not required.

- Record keeping requirements.

Suspended July 1, 2010, through June 31, 2013.

For questions about the exemption, call Kurt Sand at (360) 705-6659.

- Sales/Use tax exemption for replacement parts for farm machinery & equipment

-

Available to:

Eligible farmers.

Qualifying activity:

Eligible farmers who purchase replacement parts for qualifying farm machinery and equipment.

As of June 14, 2014, eligible farmers will use the Farmers’ Certificate for Wholesale Purchases and Sales Tax Exemptions to obtain this exemption.

Reporting/documentation:

- Eligible farmers provide a completed Farmers’ Certificate for Wholesale Purchases and Sales Tax Exemptions to the vendor.

- No prior departmental approval required.

- No Annual Tax Performance Report.

- Electronic filing not required.

- Proper record keeping required.

For questions about the exemption, call Kurt Sand at (360) 705-6659.

Food Manufacturing Industry

- B&O tax deduction for manufacturers of dairy products

-

Available to:

Dairy product manufacturers.

Qualifying activity:

- Manufacturing dairy products (expires July 1, 2035); and

- Selling at retail or wholesale dairy products manufactured by the seller to purchasers who transport the goods out of this state (expires July 1, 2035); and

- Wholesale sales by dairy product manufacturer to a customer who uses such dairy products as an ingredient or component in the manufacturing of another dairy product in Washington (expires July 1, 2025).

Reporting/documentation:

- No application.

- Annual Tax Performance Report must be filed by May 31st of the following year.

- Electronic filing of all documents required.

For questions about the program, call Taxpayer Account Administration at 360-705-6210.

- B&O tax exemption for manufacturers and sellers of seafood products

-

Available to:

Seafood product manufacturers.

Qualifying activity:

- Manufacturing seafood products that remain in a raw, raw frozen, or raw salted state at the completion of the manufacturing by that person; and

- Selling at retail or wholesale manufactured seafood products that remain in a raw, raw frozen, or raw salted state to purchasers who transport the goods out of this state.

Reporting/documentation:

- No application.

- Annual Tax Performance Report must be filed by May 31st of the following year.

- Electronic filing of all documents required.

Expires July 1, 2035.

For questions about the program, call Taxpayer Account Administration at 360-705-6210.

- B&O tax exemption for manufacturers of fresh fruit & vegetables

-

Available to:

Manufacturers of fresh fruit and vegetables.

Qualifying activity:

- Manufacturing fresh fruits or vegetables by canning, preserving, freezing, processing, or dehydrating fresh fruits or vegetables; or

- Selling at wholesale fruits or vegetables manufactured by the seller when sold to purchasers who transport the goods out of this state.

Reporting/documentation:

- No application.

- Annual Tax Performance Report must be filed by May 31 of the following year.

- Electronic filing of all documents required.

Expires July 1, 2035.

For questions about the program, call Taxpayer Account Administration at 360 705-6210.

- Tax deferrals for fruit and vegetable businesses (expired June 30, 2012)

-

Available to:

Dairy, seafood or fresh fruit processors or cold storage warehouses owned or operated by a wholesaler or third-party warehouser to store qualifying products.

This program expired June 30, 2012. We will not accept applications.

For questions about deferrals, please email DORDeferrals@dor.wa.gov or call our Deferral Program Lead at 360-534-1443.

General Manufacturing

- Manufacturers Sales and Use Tax Deferral - Eligible Investment Projects

-

Available to:

Manufacturers constructing eligible investment projects. Applications will be accepted beginning January 1, 2018. The application must be submitted before initiation of construction or acquisition of equipment. Only two new manufacturing facilities per calendar year can be approved, one of which much be located in eastern Washington and one of which must be located in western Washington.

Note: This is a deferral, not an exemption or waiver. The recipient must begin paying the deferred taxes in the fifth year after the date on which the investment project has been operationally completed.

Qualifying activity:

Construction of an eligible investment project by a manufacturer.

"Eligible investment project" means an investment project for qualified buildings and machinery and equipment on two new, renovated, or expanded manufacturing operations per year, at least one of which must be located east of the crest of the Cascade mountains, and one of which must be located west of the crest of the Cascade mountains. The deferral provided in this section only applies to the state and local sales and use taxes due on the first ten million dollars in costs for qualified buildings and machinery and equipment.

Reporting/documentation:

- Application required.

- Annual Tax Performance Report must be filed electronically by May 31 of the following year in which the project is operationally complete and for the following seven years.

- Buyer’s Sales and Use Tax Preference Addendum in My DOR is required when filing your Excise Tax Returns. The addendum is found by selecting “Yes” under “Do you need to file a Buyer’s Sales and Use Preference Addendum?” on the Summary page of the return.

- Electronic filing required.

For questions about deferrals, please email DORDeferrals@dor.wa.gov or call our Deferral Program Lead at 360-534-1443.

- Sales and Use Tax Exemption for Manufacturing Machinery & Equipment (M&E)

-

Available to:

Manufacturers and processors for hire performing manufacturing and R&D. Testing operation for a manufacturer and processor for hire.

Qualifying activity:

Purchase of qualifying machinery and equipment used directly in a manufacturing operation or research and development performed by a manufacturer, or testing operations performed for a manufacturer.

Reporting/documentation:

- Completion of Manufacturers’ Sales and Use Tax Exemption Certificate for vendor.

- No application.

- No Annual Tax Performance Report.

- Electronic filing not required.

For questions about the exemption, call 360-705-6705.

Resources

Manufacturing Industry Tax Guide (pdf)

Manufacturer's Sales/Use Tax Exemption (pdf)

RCW

WAC

ETA

- Sales/use tax deferral - Manufacturing and research and development in qualifying counties

-

Available to:

Manufacturers and research and developers located in counties with a population of less than 650,000 at the time of application. Applications will be accepted starting July 1, 2022. The application must be submitted before initiation of construction or purchase of equipment.

Note: This is a deferral, not an exemption. However, you do not have to repay deferred taxes unless you do not meet the conditions of the deferral program.

Qualifying activity:

Construction of qualified building and/or qualified machinery and equipment by a manufacturer and/or research and developer. The amount of sales/use tax that can be deferred is limited to $400,000 per person.

Program requirements:

The application must be submitted before initiation of construction or purchase of machinery and equipment.

The recipient of a deferral certificate must begin meaningful construction on an eligible investment project within two years of receiving the certificate. If the recipient does not begin meaningful construction within two years of receiving the deferral certificate, the certificate is invalid and taxes are due immediately.

Repayment of deferred taxes:

You do not have to repay the deferred taxes unless one of the following occurs:

- The project is not operationally complete within five years of the issuance of the certificate.

- The project is used in a non-qualifying manner at any time during the deferral period.

A portion of the tax is due if the Annual Tax Performance report is not submitted timely.

Reporting/documentation:

- Application required.

- Annual Tax Performance Report must be filed electronically by May 31 of the year after the project is certified and for the next seven years.

- Buyers must also complete the Buyer’s Sales and Use Tax Preference Addendum when filing their excise tax returns.

- Electronic filing required.

Applications will not be accepted after June 30, 2032.

For questions about deferrals, please email DORDeferrals@dor.wa.gov or call our Deferral Program Lead at 360-534-1443.

High Technology Industry

- Biotechnology & medical device manufacturing sales & use tax deferral/waiver (expired January 1, 2017)

-

Available to:

Biotechnology and medical device manufacturers.

This program expired January 1, 2017. We will not accept applications.

For questions about deferrals, please email DORDeferrals@dor.wa.gov or call our Deferral Program Lead at 360-534-1443.

- High technology sales & use tax deferral/waiver (expired January 1, 2015)

-

Available to:

Limited to businesses conducting R&D and pilot scale manufacturing in the fields of:

- Advanced computing.

- Advanced materials.

- Biotechnology.

- Electronic device technology.

- Environmental technology.

This program expired January 1, 2015. We will not accept applications.

For questions about deferrals, please email DORDeferrals@dor.wa.gov or call our Deferral Program Lead at 360-534-1443.

High Unemployment County/CEZ

- High unemployment county sales and use tax deferral for manufacturing facilities (expired July 1, 2020)

-

Available to:

Manufacturers or businesses that conditions vegetable seeds, research and development and commercial testing for manufacturers in an eligible county or in a Community Empowerment Zone (CEZ).

This program expired July 1, 2020. We will not accept applications.

For questions about deferrals, please email DORDeferrals@dor.wa.gov or call our Deferral Program Lead at 360-534-1443.

Leasehold Excise Tax (LET)

- LET exemption for arenas with a seating capacity of more than 4,000

-

Available to:

Public or entertainment arenas, effective October 1, 2023.

Qualifying activity:

- The arena has seating capacity of more than 4,000;

- The arena is located on city-owned land;

- The arena is located within a city with a population over 100,000; and

- Private entities were responsible for 100% of the cost of constructing improvements to the arenas, which were not reimbursed by the public owner.

Reporting/documentation:

- No application required.

- Annual Tax Performance Report filed by May 31 of the following year.

- Electronic filing of all documents required.

Expires January 1, 2034.

For questions about the credit, call Taxpayer Account Administration at 360-705-6115.

Miscellaneous Incentive Programs

- B&O Tax/Public utility tax credit for electricity, natural gas, or manufactured gas sold to silicon smelters

-

Available to:

A person who sells electricity, natural gas or manufactured gas to a silicon smelter in Washington State.

Qualifying activity:

To qualify for the credit a person must sell electricity, natural gas, or manufactured gas to a silicon smelter. The credit is equal to the gross amount of sales to the aluminum smelter by the corresponding rate of Business and Occupation (B&O) Tax and/or Public Utility Tax (PUT). However, this is only when it’s specified in a contract that the price of the electricity or gas sold to the smelter will be reduced by an amount equal to the credit.

Reporting/documentation:

File a quarterly report that includes

- Volume of gas delivered.

- Consumer’s name.

- Other information.

No Annual Tax Performance Report required.

Electronic filing not required.

- Commute trip reduction program - B&O tax/public utility tax credit (expired July 1, 2025)

-

Available to:

Employers and property managers. The accrual period for a property manager that provides incentives to persons employed at a worksite managed by the property manager expired on December 31, 2023.

Qualifying activity:

Providing commute trip reduction incentives to or on behalf of employees.

Reporting/documentation:

- Applications no longer accepted as of January 31, 2025.

- Credit must be claimed electronically through My DOR.

Program expired July 1, 2024, for property managers, and July 1, 2025, for employers. No credits may be applied to returns filed after June 30, 2025, even if they relate to prior tax periods.

- Employee Ownership B&O Credit (Repealed July, 2025)

-

Available to:

Businesses converting to an employee ownership structure.

Qualifying activity:

Converting your business to any of the following employee ownership structures:

- Worker-owned cooperative.

- Employee ownership trust.

- Employee stock ownership plan.

Credit amount:

The credit is equal to:

- Up to 50%, but no more than $25,000, of the costs of converting to a worker-owned cooperative or an employee ownership trust.

- Up to 50%, but no more than $100,000, of the costs of converting to an employee stock ownership plan.

If approved, you may claim the credit on your excise tax return starting in the reporting period when the conversion is complete. You may carry forward any unused credit for up to 12 months. The credit cannot exceed your B&O tax liability, and the department cannot issue refunds.

Credit cap and end date:

- Credits are available on a first-in-time basis.

- Credits can be earned through June 30, 2025.

- No credits can be claimed for filing periods on or after July 1, 2026.

- No credits can be approved after the statewide annual cap of $2,000,000 has been met

Reporting/documentation:

- Apply online through My DOR.

- No Annual Tax Performance Report.

For questions, call Taxpayer Account Administration at 360-705-6214.

Statewide annual credit taken in 2024

Applied for: $200,000.00

Amount issued: $200,000.002025 Statewide annual credit balances

(As of September 2, 2025)Applied for: $0

Amount issued: $0

Remaining available: $2,000,000.00 - Equitable Access to Credit Program - B&O tax credit

-

Available to:

Persons who make qualified contributions.

Qualifying activity:

Contributions made to the Equitable Access to Credit Program through the Department of Commerce.

Reporting/documentation:

- Contributions must be made before credit is claimed.

- No application required.

- Electronic filing of all documents required.

- File an Annual Tax Performance Report by May 31st of the following year.

No credit may be earned for contributions made after June 29, 2027.

No credit may be claimed on returns filed after December 31, 2029.

For questions about the credit, call Taxpayer Account Administration 360-705-6214.

Resources

Special Notice - Equitable Access to Credit Program B&O tax credit

RCW

Effective June 9, 2022 (E2SHB 1015, Chapter 189, Laws of 2022).

- International services - B&O tax credit for new employment

-

Available to:

Persons providing international services, such as computer; data processing; information; legal; accounting and tax preparation; engineering; architectural; business consulting; business management; public relations and advertising; surveying; geological consulting; real estate appraisal; or financial services in designated geographical areas.

Qualifying activity:

Creating permanent full-time positions in international services located in a Community Empowerment Zone (CEZ) or designated International Services District. International services must be provided to persons domiciled outside the United States or be for use primarily outside this country.

Credit amount:

$3,000 per year for each qualified employment position created. Additionally, $3,000 in credit can be taken in each of the following four years if the position is maintained.

Reporting/documentation:

- No application.

- No Annual Tax Performance Report.

- Electronic filing not required.

- Maintain records necessary for the department to verify eligibility:

- Employment records for the previous six years;

- Information relating to description of international service activity engaged in at the eligible location by the person; and

- Information relating to customers of international service activity engaged in at that location by the person.

For questions about the credit, call Taxpayer Account Administration at 360-705-6214.

- Main street tax credit - B&O tax/public utility tax credit

-

Available to:

All businesses that meet both of the following requirements:

- Complete the required application through My DOR. Learn more about how to apply.

- Once approved, make contributions to the designated Main Street Organization(s) and/or the Main Street Trust Fund.

Contribution deadlines:

A business must make the total approved contribution to the designated Main Street Organization or Main Street Trust Fund by Nov. 15 of the same year they applied for the credit. If a business misses the Nov. 15 deadline, the credits are forfeited and become available to new applicants.

A business that is approved after Nov. 15, must make the total contribution by the end of the calendar year in which the contribution was approved.

How to use the credit

Credit(s) earned will be available for use on excise tax return(s) the following calendar year. To use the credit, a business must have a B&O tax or a public utility tax liability equal to or exceeding the amount of the credit. Credits cannot be carried forward to the next calendar year or refunded.

Credit limits

Businesses

The total amount of credit claimed in any calendar year may not exceed the lesser of either:

- The approved credit.

- 75% of the contribution made to a Main Street Organization and 75% of the contribution made to the main street trust fund in the prior calendar year.

A business may not exceed $250,000 in total credits during a calendar year.

Organizations

Each year between the second Monday of January through March 31, the department evenly allocates the credits allowed by dividing the statewide cap of $5 million by the number of eligible Main Street Organizations and the Main Street Trust Fund.

Example: Assuming there are 33 Main Street Organizations including the Main Street Trust Fund, the first quarter cap is limited to $151,515 = ($5 million/33).

On April 1 of each year, if funds are still available under the statewide cap, the credits allowed for contributions to an individual organization can total up to $160,000.

On October 1 of each year, if funds are still available under the statewide cap, individual organizations may receive additional contributions. The total amount of credits arising from contributions received by any organization may not exceed $250,000 annually.

Reporting/documentation

- No Annual Tax Performance Report.

- Electronic filing of all documents required.

Expires Jan. 1, 2032.

For questions about the application, call Taxpayer Account Administration at 360-705-6214.

- Motion Picture Competitiveness Program B&O tax credit (formerly known as Washington Filmworks Contributors B&O Tax Credit)

-

Available to:

All persons that make qualified contributions.

Qualifying activity:

Cash contributions made to an approved Motion Picture Competitiveness Program (such as Washington Filmworks).

Reporting/documentation:

- Credit may be claimed for contributions made from June 7, 2012, through June 30, 2030.

- Contributions must be made before credit is claimed.

- No application required. Electronic filing of all documents required.

- Effective July 23, 2023, contributors who receive funding assistance through the Motion Picture Competitiveness Program are no longer required to file an Annual Tax Performance report.

No credit may be earned for contributions made on or after July 1, 2030.

No credits may be claimed on returns filed after December 31, 2033.

For questions about the credit, call Taxpayer Account Administration 360-705-6214.

- Newspapers - reduced B&O tax rate for publishers

-

Note: The reduced B&O tax rate is replaced by an exemption effective January 1, 2024.

Available to:

Printers and/or publishers of newspapers as defined in RCW 82.04.214.

Qualifying activity:

The reduced rate of 0.35 percent applies to gross income from printing and/or publishing of newspapers until December 31, 2023.

Reporting/documentation:

- No application.

- Annual Tax Performance Report must be filed by May 31 of each year following a year when you claimed the incentive.

- Electronic filing of all documents required.

Note: Printers and/or publishers of newspapers must also report Litter tax on the value of newspapers printed and/or sold in Washington.

Expires Dec. 31, 2023.

For questions about the reduced rate, call Taxpayer Account Administration at 360-705-6214.

- Newspapers – B&O tax exemption

-

Available to:

Businesses primarily engaged in printing and/or publishing of newspapers or eligible digital content.

Qualifying activity:

The exemption applies to gross income from printing and/or publishing of newspapers or eligible digital content.

Note: The exemption must be reduced by an amount equal to any expenditures made by the business during the reporting period. “Expenditure” includes a payment, contribution, subscription, distribution, loan, advance, deposit, or gift of money or anything of value, and includes a contract, promise, or agreement, whether or not legally enforceable, to make an expenditure.

Expenditure also includes a promise to pay, a payment, or a transfer of anything of value in exchange for goods, services, property, facilities, or anything of value for the purpose of assisting, benefiting, or honoring any public official or candidate, or assisting in furthering or opposing any election campaign.

Expenditures shall not include the partial or complete repayment by a candidate or political or incidental committee of the principal of a loan, the receipt of which loan has been properly reported.Reporting/documentation:

- No application.

- Annual Tax Performance Report must be filed by May 31 of each year following a year when you claim an incentive.

- Electronic filing of all documents required.

Note: Printers and/or publishers of newspapers must also report Litter tax on the value of newspapers printed and/or sold in Washington.

Expires Jan. 1, 2034.

For questions about the exemption, call Taxpayer Account Administration at 360-705-6214.

- Power for electrolytic processing - public utility tax exemption

-

Who qualifies for this exemption?

You can qualify for a public utility tax exemption if you are a light and power business that provides electricity to qualifying electrolytic processing businesses. This exemption expires July 1, 2029. You can only use the exemption for electricity sales you make on or before December 31, 2028.

What is a qualifying electrolytic processing business?

A qualifying electrolytic processing business is a business that uses more than 10 average megawatts of electricity per month to split the chemical bonds of sodium chloride and water in one of the following ways:

- Using the chlor-alkali electrolytic process to make chlorine and sodium hydroxide; or

- Using the sodium chlorate electrolytic process to make sodium chlorate and hydrogen.

As of June 10, 2004, sales of electricity to electrolytic processing businesses that contract for power from the Bonneville power administration, do not qualify for this exemption.

How to qualify for an exemption:

As a light and power business, you can qualify for a public utility tax exemption on your sales of electricity made to a qualifying chlor-alkali electrolytic processing business or a sodium chlorate electrolytic processing business for the electrolytic process if the contract for the sale contains all the following terms:

- The electricity that the business uses in the electrolytic process must be metered separately from the electricity the business uses for general operations;

- You reduce the price for the electricity used in the electrolytic process by an amount equal to the tax exemption available to you; and

- If you disallow all or part of the exemption, that is a breach of contract and the damages the electrolytic processing business pays are the amount of the tax exemption you disallowed.

You cannot use this exemption for amounts you receive from the remarketing or resale of electricity that an electrolytic processor originally obtained by contract.

How to report:

- Both the buyer and the seller must complete a Public Utility Tax Exemption Certificate for Persons Supplying Power to Electrolytic Processor.

- The buyer must file the Annual Tax Performance Report by May 31 of the following year.

- You must file all documents electronically.

For questions about the program, call 360-705-6705.

- Sales/Use tax deferral – Affordable housing on underdeveloped lands

-

Available to:

Owners of underdeveloped land building affordable housing in a qualifying city.

Underdeveloped property means land used as a surface parking lot for parking motor vehicles off the street or highway, that is open to public use with or without charge.

A qualifying city is a city with a population of at least 135,000 but not more than 250,000 at the time the city initially establishes the program.

Applying for a deferral:

An application must be submitted before initiation of construction. Applications will not be accepted after June 30, 2032.

You must have a conditional certificate of approval from a qualifying city, or your application will be denied.

Deferral Program requirements:

The investment project must be completed within three years of approval of the application. Additionally, the investment project requires occupancy of 50% or more of the project by qualified households starting in the year the certificate of occupancy is issued, plus the next nine years.

Paying deferred taxes:

If all program requirements have been met, the deferred sales/use tax is waived by the department after the tenth year.

If requirements are not met, the deferred taxes are due.

Reporting/documentation:

- Application required.

- Buyer must provide seller with a copy of the deferral certificate.

- Annual Tax Performance Report filed by May 31 of the year after the certificate of occupancy is issued, and for the next 9 years.

Note: If you have income that requires you to file excise tax returns, you must also complete the Buyer’s Sales and Use Tax Preference Addendum.

Deferral program expires July 1, 2032.For questions about deferrals, please email DORDeferrals@dor.wa.gov or call our Deferral Program Lead at 360-534-1443.

More information

Other resources

- Sales/Use tax deferral – Multifamily housing from existing buildings

-

Available to:

Owners of underutilized commercial property with properties located in cities that have an approved deferral program to convert such properties into qualifying multifamily housing.

Underutilized commercial property means an entire property, or portion thereof, currently used or intended to be used by a business for retailing or office-related or administrative activities.

Multifamily housing means a building or a group of buildings having four or more dwelling units not designed or used as transient accommodations and not including hotels and motels. Multifamily units may result from rehabilitation or conversion of vacant, underutilized, or substandard buildings to multifamily housing.

Applying for a deferral:

An application must be submitted before initiation of construction. Applications will not be accepted after June 30, 2034.

You must have a conditional certificate of approval from the city, or your application will be denied.

Deferral program requirements:

- The investment project must be completed within three years of approval of the application unless an extension is granted by the city or town.

- The investment project must be primarily for multifamily housing units.

- At least 10% of the units must be affordable housing for low-income households.

- In a mixed-use project, only the ground floor of a building may be used for commercial purposes with the remainder dedicated to multifamily housing units.

Additional requirements may be added by the city. These requirements must be met in the year the certificate of occupancy is issued, plus the next nine years.

Paying deferred taxes:

If all program requirements have been met, the deferred sales/use tax is waived by the department after the tenth year.If requirements are not met, the deferred taxes plus interest are immediately due and payable.

Reporting/documentation:

- Application required.

- Buyer must provide seller with a copy of the deferral certificate.

- Annual Tax Performance Report filed by May 31 of the year after the certificate of occupancy is issued, and for the next 9 years. Annual tax filers are not required to file an annual tax performance report.

Note: If you have income that requires you to file excise tax returns, you must also complete the Buyer’s Sales and Use Tax Preference Addendum.

Deferral program expires July 1, 2034.

For questions about this deferral program email us at RulingsDOR@dor.wa.gov.

For general questions about deferrals, please email DORDeferrals@dor.wa.gov or call our Deferral Program Lead at 360-534-1443. - Sales/Use tax exemption for motion picture and video production companies on rental of production equipment and purchase of production services

-

Available to:

Motion picture and video production companies.

Qualifying activity:

Rental of production equipment. The exemption does not extend to the purchase of production equipment.

Reporting/documentation:

- Purchaser provides seller with completed Motion Picture And Video Production Business Exemption Certificate or Buyer’s Retail Sales Tax Exemption Certificate.

- No application required.

- No Annual Tax Performance Report.

Electronic filing not required

For questions about the exemption, call Taxpayer Account Administration at 360-705-6214.

- Weatherization assistance program - sales & use tax exemption

-

Available to:

Department of Commerce weatherization program contractors.

Qualifying activity:

Purchase of tangible personal property that becomes a component part of a qualifying residence under the weatherization program administered by Department of Commerce.

Examples of qualifying weatherization materials include, but are not limited to the following:

• Insulation and sealants

• Parts for air infiltration

• Heating and cooling equipment

• Supplies used to seal and repair ductsNote: Charges for labor and services used to install these materials continue to be subject to sales tax and use tax.

Reporting/documentation:

- Completion of Buyers’ Retail Sales Tax Exemption Certificate by contractor for vendor.

- Check 6(q).

- No application required

- No Annual Tax Performance Report

Electronic filing not required

For information on the weatherization program, contact Department of Commerce.

- Completion of Buyers’ Retail Sales Tax Exemption Certificate by contractor for vendor.

Renewable Energy/Green Incentives

- Anaerobic digesters - property and leasehold excise tax exemption (expired Dec. 31. 2024)

-

The department cannot accept applications for these exemptions as of Dec. 31, 2024.

Was available to:

Owners and operators of anaerobic digesters.

What qualified for an exemption:

Property used primarily to operate an anaerobic digester such as:

- Buildings, machinery, equipment, and other personal property.

- Land on which the property is located.

- Land necessary to operate the anaerobic digester (does not include land used to grow agricultural products).

The exemption could be used for six assessment years after the date the facility or addition became operational.

Reporting/documentation:

- No Annual Tax Performance Report required.

You cannot apply for these exemptions after Dec. 31, 2024.

- Clean alternative fuel and plug-in hybrid vehicles - sales/use tax exemptions (expired July 31, 2025)

-

Beginning Aug. 1, 2019, a sales and use tax exemption for new or used clean alternative fuel and certain plug-in hybrid vehicles is available. The Department of Licensing maintains a list of qualifying vehicles.

Qualifying vehicles

The exemption is applied to the sales price or fair market value when you purchase or lease a passenger car, light duty truck, or medium duty passenger vehicle that is powered exclusively by a clean alternative fuel or capable of traveling at least 30 miles using only battery power.

In addition, the vehicle must be sold or valued at $45,000 or less if new and $30,000 or less if used.

Manufacturer and distributor rebates are part of the selling price. The amount of the rebate is not allowed to be used in any way to reduce the sales price or value.

The selling price includes delivery charges or any other services necessary to complete the sale (RCW 82.08.010).

Dealers may not deduct the value of any trade-in vehicle or any federal tax credits that may accrue to the lessor when determining exemption eligibility.

Exemption amounts

For qualified vehicles, the exempted amount is determined as follows:

New vehicles purchased

Sales or use tax exemption available

Aug. 1, 2019 - July 31, 2021

Up to $25,000 of the sales or lease price

Aug. 1, 2021 - July 31, 2023

Up to $20,000 of the sales or lease price

Aug. 1, 2023 - July 31, 2025

Up to $15,000 of the sales or lease price

Used vehicles purchased Sales or use tax exemption available Aug. 1, 2019 - July 31, 2025 Up to $16,000 of the sales or lease price Purchasing from an auto dealer

The auto dealer you purchase or lease the vehicle from must keep records to support the exemption. You, the buyer, do not need to report the exemption.

Requesting a sales or use tax refund

You may apply to the Department of Revenue by submitting an application for refund of use tax or refund of sales tax, if you paid sales or use tax in error between Aug. 1, 2019 and July 31, 2025.

Sales and use tax exemptions expiration dates

- The exemption for sales of new and used qualifying vehicles expired July 31, 2025.

- Leases that qualify for this exemption on or before July 31, 2025, can continue to claim the exemption on lease payments due through July 31, 2028.

- Note: You must use the "Other" deduction with a description such as "Lease payment under RCW 82.08.809."

For questions about the exemption, call 360-705-6705.

Resources

Green transportation sales tax refund request (pdf)

RCW

82.08.809

82.08.9999

82.12.809

82.12.9999WAC

- Clean alternative fuel commercial vehicle and vehicle infrastructure B&O or PUT tax credit

-

Available to:

Businesses that use commercial vehicles to transport commodities, merchandise, produce, refuse, freight, animals or passengers, using vehicles that use clean alternative fuel. The vehicle must display a WA license plate.

Qualifying activity:

Purchases or leases of new commercial vehicles and qualifying used commercial vehicles with propulsion units that are principally powered by a clean alternative fuel. This includes:

- Costs to modify a commercial vehicle to be principally powered by a clean alternative fuel, including parts incorporated into the vehicle and labor or service charges to modify the vehicle.

- Purchases of alternative fuel vehicle infrastructure component parts, as well as related installation and construction costs.

Credit is not earned on vehicles purchased to lease to others.

Refer to the Special Notice Clean alternative fuel commercial vehicles and vehicle infrastructure tax credits expanded for information on how to calculate the credit, caps, and application dates.

Reporting/documentation requirements:

- No Annual Tax Performance Report.

- Electronic filing required.

- Apply for the Commercial Vehicle Credit and/or Alternative Fuel Vehicle Infrastructure Credit (3 part application) in MyDOR.

Statewide annual credit balances

(As of October 8, 2025)Applied for: $1,417,158.94

Amount issued: $1,631,051.27

Remaining available: $4,368,948.73Statewide total credit balances

(From July 15, 2015 through September 2, 2025)Applied for: $24,036,026.92

Amount issued: $17,875,062.00

Remaining available: $14,624,938.00Statewide annual credit approved in 2024 was $822,739.98.

Note: The remaining available credit is the total annual statewide cap less any credits issued.

For questions about the application, call Taxpayer Account Administration at 360-705-6214.

- Electric vehicle infrastructure (charging stations), batteries, and fuel cells – sales/use tax exemption, leasehold tax exemption (expired July 1, 2025)

-

Available to:

Anyone who purchases an electric vehicle battery or fuel cell, or installs an electric vehicle battery, fuel cell charging station, or hydrogen fueling stations.

Electric vehicle infrastructure means structures, machinery, and equipment necessary and integral to support an electric vehicle, including battery charging stations, rapid charging stations, battery exchange stations, fueling stations that provide hydrogen for fuel cell electric vehicles, renewable hydrogen production facilities, and (as of June 9, 2022) green electrolytic hydrogen production facilities.

Qualifying activity:

- The sale or use of batteries and fuel cells for electric vehicles, including those sold as a component of an electric bus.

- The sale of or charge made for labor and services rendered in respect to installing, repairing, altering, or improving electric vehicle batteries and fuel cells.

- The sale of or charge made for labor and services rendered in respect to installing, constructing, repairing, or improving battery or fuel cell electric vehicle infrastructure, including hydrogen fueling stations.

- The sale or use of tangible personal property that will become a component of battery or fuel cell electric vehicle infrastructure during the course of installing, constructing, repairing, or improving battery or fuel cell electric vehicle infrastructure.

Reporting/documentation:

- Buyer must give the vendor a completed Buyers’ Retail Sales Tax Exemption Certificate.

- Sellers must report the exempt sales on their excise tax returns and take the corresponding deduction from retail sales tax.

Leasehold excise tax exemption:

- An exemption from leasehold excise tax is allowed on leases to tenants of public lands for the purpose of installing, maintaining, and operating electric vehicle infrastructure.

Expired July 1, 2025.

For questions about the exemptions, call 360-705-6705.

- Electric vessel and marine batteries and shoreside infrastructure sales/use tax exemption

-

Available to:

Anyone who purchases qualifying batteries or shoreside infrastructure.

Qualifying activity:

Beginning July 1, 2020, purchases of:

- Batteries and battery packs used to power electric marine propulsion systems or hybrid electric marine propulsion systems with a continuous power greater than 15 kW.

- New shoreside batteries purchased and installed for the purpose of reducing grid demand when charging electric and hybrid vessels.

- The labor and services rendered in respect to installing, repairing, altering, or improving marine batteries or battery packs, or shoreside batteries and shoreside battery infrastructure.

Buyers:

- Complete a Buyer’s retail sales tax exemption certificate for the vendor.

- If you are a registered business, you must also complete the buyer’s tax preference addendum in My DOR when filing your excise tax return.

Sellers:

- When reporting such sales on your excise tax return, use deduction, "Sales of Batteries / Infrastructure for Electric and Hybrid Vessels."

Expires July 1, 2030.

For questions about the program, call 360-705-6705.

- Electric vessel and marine propulsion system sales/use tax exemption

-

Available to:

Anyone purchasing qualifying new vessels or qualifying new marine propulsion systems.

Qualifying activity:

Beginning Aug. 1, 2019, purchases of:

- New vessels equipped with battery-powered electric marine propulsion systems with continuous power greater than 15 kW.

- New battery-powered electric marine propulsion systems with continuous power greater than 15 kW.

Buyers:

- Complete a Buyer’s retail sales tax exemption certificate for the vendor.

- If you are a registered business, you must also complete the buyer’s tax preference addendum in My DOR when filing your excise tax return.

Sellers:

- When reporting such sales on your excise tax return, use deduction "Sales of New Electric Vessels and Marine Propulsion Systems."

Expires July 1, 2030.

For questions about the program, call 360-705-6705.

- Hog fuel sales & use tax exemption

-

Available to:

Purchasers of hog fuel. Hog fuel is defined as wood waste and other wood residuals including forest-derived biomass. It does not include firewood or wood pellets.

Qualifying activity:

Producing electricity, steam, heat, or biofuel from hog fuel.

Reporting/documentation:

- No application required.

- Completion of Buyers’ Retail Sales Tax Exemption Certificate for vendor.

- Annual Tax Performance Report by May 31st of the following year.

- Completion of Buyers Sales and Use Tax Preference Addendum in My DOR when filing their tax return.

Expires June 30, 2034.

For questions about the exemption, call 360-705-6705.

- Hydrogen fuel cell electric vehicles – sales/use tax exemptions

-

Available to:

Beginning July 1, 2022, a sales and use tax exemption is available for new or used electric vehicles powered by a hydrogen fuel cell. The Department of Licensing (DOL) maintains a list of qualifying vehicles.

Qualifying vehicles

The exemption is applied to the sales price or fair market value when you purchase or lease a passenger car, light duty truck, or medium duty passenger vehicle that is powered by a technology that uses an electrochemical reaction to generate energy by combining hydrogen and oxygen.

This exemption cannot be combined with the clean alternative fuel and plug-in hybrid vehicle exemption available under RCW 82.08.9999 and RCW 82.12.9999.

Exemption amounts

New qualifying vehicles will receive a 50% sales or use tax exemption. There is no purchase price or fair market value requirement to be eligible for this exemption. Once the Department of Revenue (DOR) determines that 650 new vehicles have qualified, the new vehicle exemption will expire after the last day of the immediately following month. New leased vehicles that qualified before the expiration date will continue to receive the exemption on lease payments.

Used qualifying vehicles will receive a 100% sales or use tax exemption up to $16,000 of the sales price or the fair market value at the inception of the lease.

Records requirement